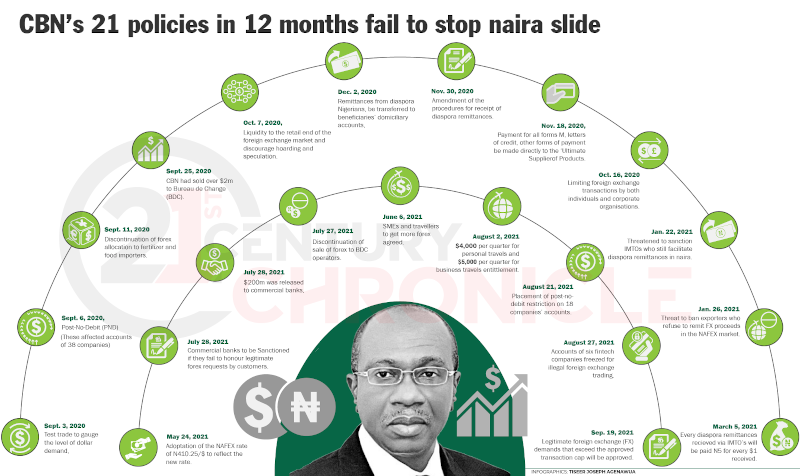

The Central Bank of Nigeria (CBN) has issued at least 21 policies and directives in the last one year – all in desperate attempts to arrest the continuous slide of the naira to no avail.

These policies and interventions, released between September 2020 and September 2021, have so far failed to stop the unprecedented depreciation of the value of the national currency.

In frantic attempts to improve liquidity in the forex market and reduce the disparity between the black market and official Import and Export (I&E) window, the CBN has come up with 100 policies between September 3, 2020 and September 19, 2021.

Despite these policies, the value of the naira has continued to decline.

The current official naira to dollar exchange rate is N410.67/$ while the rate at the parallel market is N575/$.

In the aftermath of the COVID-19 lockdown, the apex bank on September 3, in a bid to test demand and supply and the price of the naira against the dollar, in what it termed “test trade to gauge the level of dollar demand,” injected $50 million into the forexmarket. The sum of $50 million was sold to foreign investors on the spot and forward market. As at that time, the exchange rate was N447/$ at the parallel market while the official rate was N386/$.

The CBN, in a memo to commercial banks on September 6, 2020, placed a Post-No-Debit on the accounts of 38 companies, including premier Lotto, owned by Adebutu Kessington, a Nigerian businessman popularly known as “Baba Ijebu.” The move was said to be connected to illegal forex transactions. A Post-No-Debit (PND) is basically an instruction to banks not to allow any outbound transactions from the bank accounts of account owners, essentially blocking the account from outflows. The measure is usually taken for investigation and possible reclaiming of any illegal inflows into an account.

On September 11, 2020, the federal government directed the CBN to discontinue forex allocation to fertilizer and food importers.

By September 25, three weeks after it resumed forex sales, the CBN had sold over $2 million to Bureau de Change (BDC) in the country.

By October 7, 2020, forex sold by the CBN to BDCs had hit $450 million, in furtherance of efforts to inject more liquidity to the retail end of the foreign exchange market and discourage hoarding and speculation. This,however, proved inadequate to sustain initial liquidity gains as the naira closed at $458/$.

By October 16, banks reportedly began limiting foreign exchange transactions by both individuals and corporate organisations in a move said to be aimed at limiting forex transactions for the unofficial market. The Naira closed at N462/$ at this time.

On November 18, 2020, the CBN in a circular, signed by its Director for Trade and Exchange, Dr. O. S. Nnaji, while reiterating its earlier directive that destination payment for all forms M, letters of credit, and other forms of payment should be made directly to the ‘Ultimate Supplier of Products,’ gave conditions that must be met by importers if they chose to use a buying company other than the primary manufacturer.

In another circular on November 30, 2020, issued to all authorised dealers and the general public, the apex bank amended procedures for receipt of diaspora remittances. The new procedure indicated that beneficiaries of Diaspora Remittances through International Money Transfer Operators (IMTOs) could now receive such inflows in foreign currency (US Dollars) through the designated banks of their choice.

Coming closely on the heels of that memo, the CBN on December 02, in an update on the management of remittances from diaspora Nigerians, the CBN directed banks to transfer all diaspora remittances to beneficiaries’ domiciliary accounts, pay the customers in foreign currency and leave the decision of whether to be paid in cash or by transfer to the beneficiary.

In the New Year, apparently having realised that the directive on diaspora remittances had fallen through the cracks, the apex bank on January 22, 2021, threatened to sanction IMTOs who still facilitate diaspora remittances in naira.

On January 26, in a communiqué at the end of its Monetary Policy Committee (MPC) meeting, threatened to expel exporters who refuse to remit foreign exchange proceeds in the Nigerian Autonomous Foreign Exchange (NAFEX) market.

The apex bank introduced a ‘Naira for dollar’ policy on March 5, for all diaspora remittances. It said under the policy, recipients of diaspora remittances through any of its designated IMTO’s would be paid N5 for every $1 received. The policy was to end on May 8, 2021, but was later extended indefinitely.

On May 24, 2021 the CBN announced that it had adopted the NAFEX rate of N410.25/$ and updated its website to reflect the new rate, which had weakened the naira by 8 per cent. A fortnight earlier, the apex bank removed the official exchange rate of N379 to a dollar from its website, as part of moves to unify the country’s forex rates.

On June 6, CBN spokesperson, Osita Nwasonobi, in a statement, said the CBN and managing directors of Deposit Money Banks (DMBs) had agreed to Small and Medium Enterprises (SMEs) and travellers are set to get more forex as the apex banksays it will make more forex available to banks.

The apex bank said the increase in forexallocation was specifically to cater to the demands for same by small business operators and travellers and that travellers will be given the opportunity to purchaseforex for personal travel allowance (PTA), basic travel allowance (BTA), tuition fees, and medical payments and that the FOREX allocation will also cater for SMEs transactions or for the repatriation of foreign direct investment (FDI) proceeds.

On July 27, the CBN announced the discontinuation of sale of forex to BDC operators and threatened to sanction banks found doing same. The apex bank also said it would no longer license new BDC operations in the country and halted all processes for new licenses.

On July 28, $200m was released to commercial banks, following the announcement of a ban on sale of forex to Bureau De Change (BDC) operators in the country, in furtherance of efforts to meet dollar demand for legitimate end users in the country.

On July 28, the apex bank, in a circular by the director of banking supervision, Haruna Mustapha, put commercial banks on notice that they would be sanctioned if they fail to honour legitimate forex requests by customers. The banks were directed to set up teller points to meet legitimate forex demands and also warned banks to ensure that no customer is turned back or refused forexprovided documentation and other requirements are satisfied.

By August 2, commercial banks had started complying with the directive. While the dollar was selling at an official rate of N412, each traveller was said to be entitled to buy $4,000 per quarter for personal travels and $5,000 per quarter for business travels.

On August 21, the apex bank directed banks to place a post-no-debit restriction on the bank accounts of 18 companies, belonging to bureau de change firms, construction firms, property companies and investment firms.

On August 27, on the orders of a Federal High Court in Abuja, the CBN froze the accounts of six fintech companies. The bank had applied to the court requesting its approval to freeze the accounts which were being investigated for alleged “illegal foreign exchange trading,” pending the completion of investigations.

On September 17, the CBN Governor, Godwin Emefiele, said the bank will prosecute the owner of AbokiFX, OlumideOniwinde, as an illegal forex dealer for endangering the economy and manipulating exchange rates. AbokiFX is a website that publishes the parallel market exchange rate of the Naira against other currencies of the world on a daily basis.

On September 19, Emefiele said the bank will approve legitimate foreign exchange (FX) demands that exceed the approved transaction cap, provided such applications meet stipulated requirements. He spoke against the backdrop of complaints that the current FX policy which limits transactions to $5,000 may not fulfil consumers’ actual needs. He further stated that the I&E window of the CBN remains the major market which anyone seeking to procure or sell foreign exchange should patronise and urged customers to go to their banks for their FX needs, as no other rates would be recognised.

{kind=link}